Everyone says AI is in a bubble. Some compare it to 1999. They're not entirely wrong. Compressed deal timelines, detached valuations, euphoric narratives. It rhymes, as they say.

But the DotCom bubble had no geopolitical skeleton. This one does.

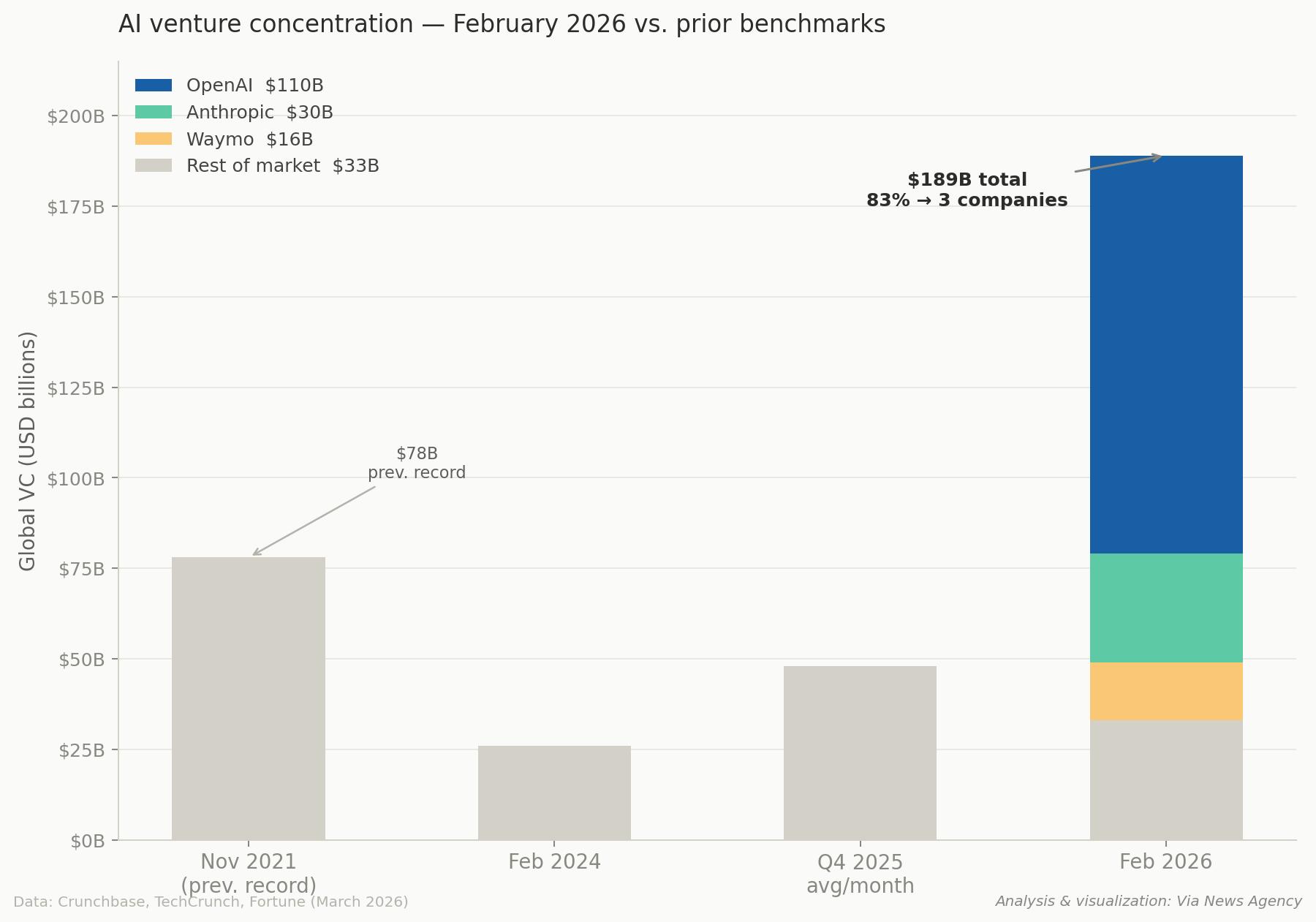

In February 2026 alone:

- OpenAI raised $110B — the largest private venture round in history

- Anthropic raised $30B — the third-largest ever

- Waymo raised $16B

Three companies. $156B. 83% of all global VC that month.

The Bifurcation

Now consider the backdrop. The same week those rounds were announced, public markets wiped out $1–2 trillion in software and tech market cap. Investors were fleeing AI-adjacent equities while simultaneously writing the largest private checks in venture history.

That looks like bifurcation.

What the Bubble Narrative Misses

The conventional bubble narrative misses three structural realities:

1. Patient Capital Requirements

R&D cycles now require patient capital that traditional venture timelines can't support — these aren't 5-year exits.

2. Sovereign-Scale Infrastructure

Infrastructure buildouts demand capital at sovereign scale — this looks more like fiber rollout economics than app store speculation.

3. Two-Tier Market Structure

The resulting two-tier market structure may actually reduce systemic risk — concentration at the top keeps the floor stable even as the long tail contracts (seed funding fell 11% YoY in February).

Insurance, Not Speculation

This looks like insurance. Smart money is buying options on not being locked out of critical infrastructure when capital becomes scarce.

Sovereign wealth funds, strategic corporates — they aren't trying to grow fast. They are positioning for the longer term.

Investment Implications

For public market investors, the implication is clear: picks-and-shovels over application layer. Nvidia, cloud providers, and energy infrastructure — not the next SaaS darling.

The bubble framing asks: when does this pop?

The better question: what happens to the countries and companies that didn't buy in and didn't get ready?

About the Chart

November 2021 was the peak of the pandemic-era venture boom. The $78B figure came largely from a cluster of massive late-stage rounds in crypto infrastructure, fintech, and SaaS — spread across hundreds of companies. It was broad-based euphoria.

Why the comparison to Feb 2026 matters:

The 2021 record was diffuse, distributed across many bets in a low-rate, risk-on environment driven by momentum and narrative.

The Feb 2026 record is the opposite: hyper-concentrated, happening during public market volatility, with rates still elevated, and led by strategic/sovereign capital rather than traditional VC.

Same headline number logic, completely different underlying structure.

That's actually the sharpest rebuttal to the bubble comparison. 2021 was a bubble dynamic. Feb 2026 looks more like a directed infrastructure bet.